Welcome to the United Nations

Welcome to the United Nations

- Rising headline inflation primarily reflects higher energy prices, amid a modest recovery in global demand

- Stronger-than-expected fourth quarter growth in Canada, China and India

- Argentina and Brazil are set to emerge from recession

Global issues

Shifting global inflation dynamics

As highlighted in the World Economic Situation and Prospects (WESP) 2017 report released in January, the trend of extremely low inflation rates has been a persistent concern for policymakers, particularly in developed economies and parts of Asia.

A prolonged period of extremely low inflation can have significant adverse effects on economic activity. One of them is the increased risk of a debt-deflation spiral: As debt is fixed nominally, very low inflation or deflation increases the real burden of the debt for borrowers. In other words, as prices decline, revenues decline but debt service remains unchanged. As a result, Governments and firms have to spend an increasing share of their revenues on servicing their existing debt obligations, forcing them to reduce spending on goods and services. Collectively, this will dampen overall demand in an economy, in turn intensifying deflationary pressures.

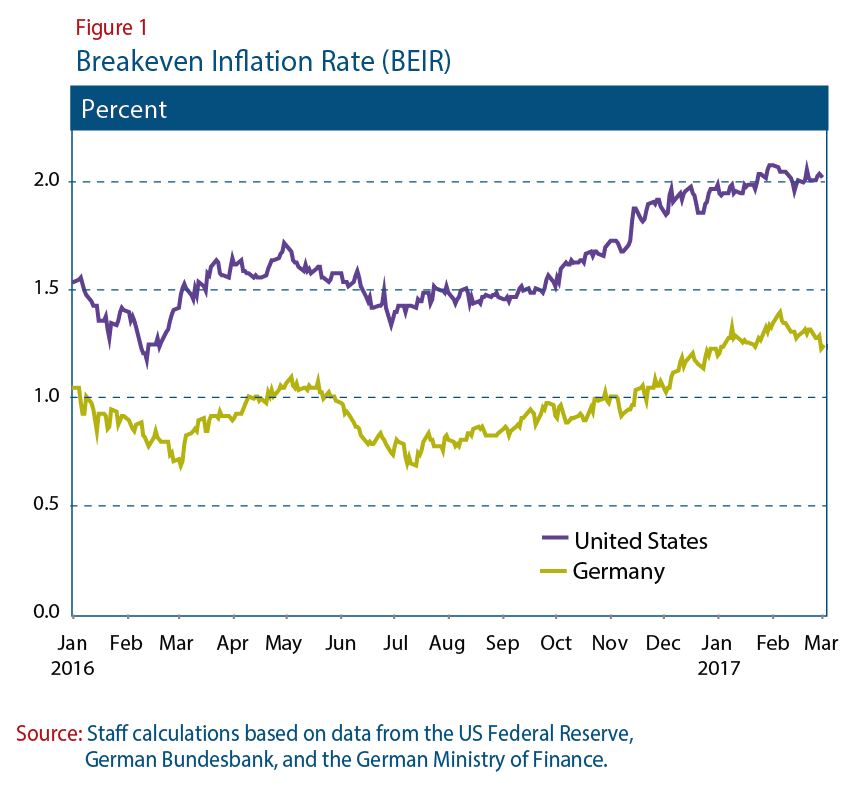

However, global inflation dynamics are changing. In February, Germany?s headline inflation increased to 2.2 per cent, the highest rate since August 2012. Similarly, headline inflation in the United States of America reached a near five-year high of 2.5 per cent in January.

Figure 1 shows the breakeven inflation rate (BEIR) for both Germany and the United States between January 2016 and February 2017. As a measure of inflation expectations, the BEIR is based on the yield difference between 10-year government bonds and inflation-indexed bonds of the same maturity. In both countries, inflation expectations have been rising in tandem with headline inflation. This uptick in both headline inflation and longer-term inflation expectations suggests that the risks associated with the extremely low inflation or prolonged deflation have diminished.

Figure 1 shows the breakeven inflation rate (BEIR) for both Germany and the United States between January 2016 and February 2017. As a measure of inflation expectations, the BEIR is based on the yield difference between 10-year government bonds and inflation-indexed bonds of the same maturity. In both countries, inflation expectations have been rising in tandem with headline inflation. This uptick in both headline inflation and longer-term inflation expectations suggests that the risks associated with the extremely low inflation or prolonged deflation have diminished.

Energy prices contributed the bulk of variation in headline inflation

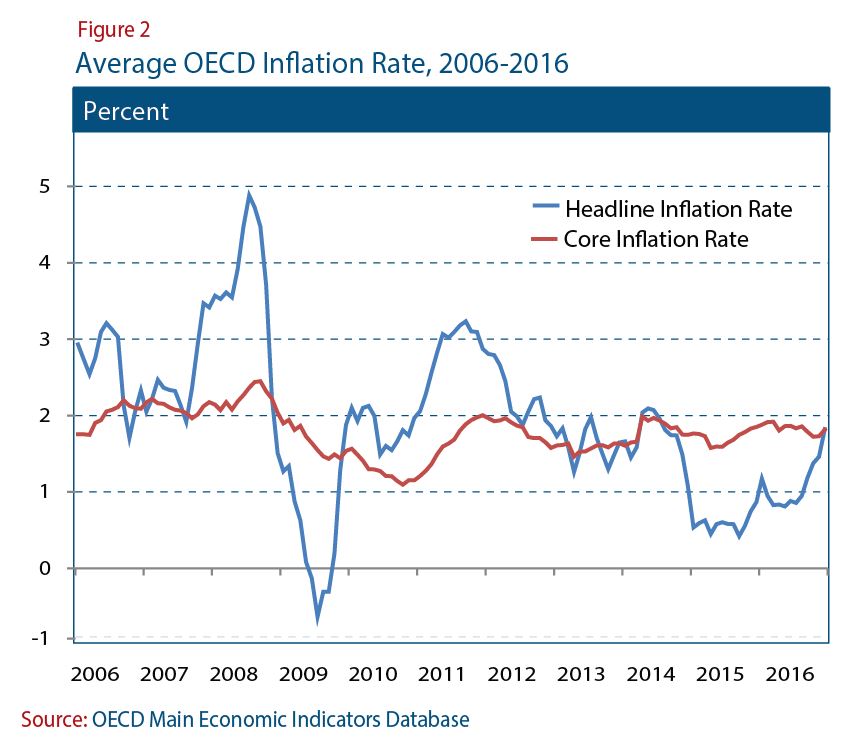

While the observed acceleration of inflation and inflation expectations in Germany and the United States points to lower risks of a debt-deflation spiral, some deflationary pressures persist. Figure 2 shows the OECD?s average core and headline inflation rates from 2006 to 2016. While movements in headline inflation have been volatile, average core inflation has been relatively stable. This implies that recent inflation dynamics have been largely influenced by energy prices, rather than aggregate demand. As headline inflation rises in tandem with oil prices, global inflation dynamics could be highly influenced by rebalancing prospects in the oil market.

A Principal Component Analysis reinforces this assertion. It shows that in OECD countries, both energy price and headline inflation have a dominating common or ?global? factor, as compared to domestic or country-specific factors. For the 2006-16 period, 73 per cent of the variation in energy inflation and 60 per cent of the variation in headline inflation can be attributed to movements in this common factor. In contrast, core inflation trends across countries were not primarily driven by a common factor, but instead by country-specific factors, including policy and economic parameters.

A Principal Component Analysis reinforces this assertion. It shows that in OECD countries, both energy price and headline inflation have a dominating common or ?global? factor, as compared to domestic or country-specific factors. For the 2006-16 period, 73 per cent of the variation in energy inflation and 60 per cent of the variation in headline inflation can be attributed to movements in this common factor. In contrast, core inflation trends across countries were not primarily driven by a common factor, but instead by country-specific factors, including policy and economic parameters.

Policymakers still need to be cautious amid subdued demand pressures

These results imply that the recent rise in headline inflation alone is not a clear sign that the world economy has escaped the risk of a debt-deflation spiral. The increase in headline inflation rates has been strongly influenced by the recovery in energy and food prices. As both energy and food prices are forecast to stabilize in the course of 2017, the pass-through to core inflation may remain limited. The common underlying trend in core inflation remained subdued in 2016. Headline inflation rates may thus not adequately reflect the state of aggregate demand. Moreover, the continuing issue of non-performing loans in Europe indicates that the region is still exposed to the risk of debt-deflation. Even in the United States, where the Federal Reserve has been on the path towards monetary policy normalization, weak wage growth suggests that fragile aggregate demand remains a concern.

Developed economies

United States: Multinational enterprises supporting employment growth

The headline unemployment rate in the United States declined to 4.7 per cent in February 2017, and has fluctuated within the range of 4.7 to 5.0 per cent since October 2015, in line with the ?central tendency? of the Federal Reserve?s estimates of its longer-run level. The headline figure, however, masks several deeper labour market issues facing the United States, where the labour force participation rate has declined from an average of 66 per cent prior to the financial crisis, to just below 63 per cent. This decline has been largely driven by demographic developments, particularly lower participation among young people related to an expansion of higher education, and early withdrawal from the labour force of workers over the age of 55. However, participation among the prime working-age population (aged 25-54 years old), which has risen steadily since late-2015, also remains below its pre-crisis level. It is important to note that headline unemployment only includes jobless persons who are available to take a job and have actively sought work in the past four weeks. The Bureau of Labor Statistics also reports several broader measures of labour underutilization. The broadest measure (defined as U-6) includes those who are currently neither working nor looking for work, but indicate that they want and are available for a job and have looked for work in the past 12 months, as well as those who are working part-time involuntarily. This measure stood at 9.2 per cent in February 2017. While this remains somewhat higher than the average of 8.3 per cent in 2007, it marks a significant improvement relative to the peak of over 17 per cent reached at the height of the financial crisis.

From a firm perspective, job creation in the United States by multinational enterprises (MNEs) has increased more rapidly than in other private-sector firms since the global financial crisis. While employment abroad by United States? MNEs in their foreign affiliates has also increased more rapidly over this period, the majority of United States? MNE employment (65.8 per cent) remains based in the United States.

Japan and Canada: GDP growth stronger than expected

Gross domestic product in Japan increased by 1 per cent in 2016, significantly faster than the estimate of 0.5 per cent underlying the forecasts in the WESP 2017. The stronger-than-expected growth was supported by a 5.5 per cent rise in private residential investment, buoyed by Japan?s negative interest rates, which have allowed home-loan rates to fall to an all-time low. Although government consumption expanded by a steady 1.5 per cent last year, public investment continued to decline, despite the strong boost to government investment plans announced in August 2016. An improvement in net trade contributed 0.5 percentage points to GDP growth in Japan in 2016, with exports expanding by 2.8 per cent in the second half of the year.

GDP growth in Canada was also slightly stronger than expected, recording a rise of 1.4 per cent in 2016, compared to an estimate of 1.2 per cent in the WESP 2017. Canada recorded a strong rise in government investment in the second half of 2016, supported by the fiscal expansion programme focused on investment in basic infrastructure that was announced in March 2016. As in Japan, net trade contributed positively to GDP growth in Canada, adding 0.7 percentage points. This was supported by competitiveness gains from the significant depreciation of the Canadian dollar since 2014.

Europe: A solid business climate in Germany

In Germany, the economy continues to perform solidly. The Ifo Business Climate Index reached a multi-year high in February, with strong data across sectors and components. However, this provides only a snapshot assessment of current economic conditions. Major uncertainties loom ahead, for example over the future path of Brexit, numerous elections in Europe and the direction of economic policy in the United States. In 2016, Germany registered a record current account surplus of ?266 billion (equivalent to 8.5 per cent of GDP), driven mainly by a widening trade surplus. In the United Kingdom, full-year growth for 2016 was revised down to 1.8 per cent, compared to 2.2 per cent in 2015. Household consumption was the main driver of this performance, which could pose a problem for the sustainability of the current growth path. The Brexit decision has led to a significant weakening of the pound, increasing inflationary pressures and thus negatively affecting consumers? purchasing power. In the Netherlands, household consumption has also supported the overall economic performance, with solid labour market conditions and wage increases underpinning consumer spending.

Economies in transition

CIS: Rebuilding fiscal buffers in the Russian Federation

Economic indicators for the Russian Federation have signalled favourable trends in early 2017. The manufacturing Purchasing Managers? Index (PMI) hit a seventy-month high in January, while the indicator of business services activity reached the highest level in eight years. Inflation slowed to 5 per cent in January, in part reflecting the moderately tight monetary policy stance. Amid decelerating inflation, there are tentative signs of an increase in real disposable income. GDP growth in the fourth quarter was positive quarter-on-quarter. For 2016 as a whole, the Russian economy is estimated to have contracted by 0.2 per cent. While growth is expected to move to positive territory in 2017, the industrial sector is already operating close to full capacity. Escaping the low-growth trajectory will require massive investment spending and overcoming structural bottlenecks. As a result of fiscal expenditure commitments in 2016, the Reserve Fund shrunk from about $50 billion in January 2016 to approximately $16 billion at the end of the year. The recovery in global oil prices will allow for the partial rebuilding of fiscal buffers. Amid concerns over currency appreciation, the Government has started to temporarily purchase foreign currency through the central bank when the oil price exceeds $40 per barrel. In Ukraine, the economy expanded at 4.8 per cent in the fourth quarter of 2016, driven by a recovery in housing demand and construction, bringing annual growth to over 2 per cent. However, the recent conflict-caused interruption of coal supplies to the energy and steel sectors may significantly derail the recovery. The economy of Belarus, which contracted by 2.6 per cent in 2016, has been affected by disputes with the Russian Federation over oil and gas imports. The resultant underutilization of oil refineries has led to a 0.5 per cent decline in Belarus? GDP in January. As sluggish domestic demand weighed on inflation, the National Bank of Belarus reduced its policy rate twice in early 2017. In February, the policy rate was also cut in Kazakhstan by 100 basis points.

In South-Eastern Europe, the economy of the former Yugoslav Republic of Macedonia is overcoming the negative impact of the domestic political crisis. Business and consumer confidence have improved and deposits in the banking system continue to recover. In January, the central bank further lowered its benchmark interest rate to support domestic demand.

Developing economies

Africa: Economic conditions in Egypt and Nigeria remain fragile amid high inflation and significant exchange rate pressure

Egypt and Nigeria, two of Africa?s largest economies, continue to face challenging economic conditions, in part due to continued strong downward pressure on their domestic currencies. Following the Egyptian pound?s devaluation of about 50 per cent against the US dollar in November 2016, movements in the domestic currency have been highly volatile, driven by concerns over foreign exchange shortages. The weak currency has contributed to rising consumer price inflation. In January, inflation accelerated for the third consecutive month, reaching 28.1 per cent, the highest rate since December 1989.

In Nigeria, inflationary pressures have continued to rise, with consumer prices increasing by 18.7 per cent in January, the fastest pace in twelve years. The rise in prices is associated with a 37 per cent depreciation of the Nigerian naira, since the Central Bank of Nigeria officially ended its US dollar peg in June 2016. Shortage of foreign currency has boosted parallel market rates, which exceeded the official rate by about 60 per cent in mid-February. Inflationary pressures have been further fueled by capital outflows resulting from the lack of long-term solutions to the fundamental causes of the naira?s deterioration: the decrease in oil revenues since 2014 and attacks on oil pipelines since 2016. In 2016, Nigeria?s GDP contracted by 1.5 per cent, the first annual contraction in 25 years.

East Asia: China announces further policy measures to address financial sector vulnerabilities

Recent economic indicators support the outlook for steady growth in the Chinese economy. In the fourth quarter, China?s GDP grew at a marginally faster pace of 6.8 per cent, driven mainly by the service sector, particularly consumer services. Meanwhile, the manufacturing industry continued to show signs of recovery in the first two months of 2017. Manufacturing sector PMI expanded at a stronger pace in February, supported by a pick-up in new export orders. Furthermore, the rebound in producer price inflation is likely to boost business sentiment and investment, as concerns over prolonged industrial deflation dissipate.

Nevertheless, amid a backdrop of rapid credit growth, high property prices, elevated corporate debt and large capital outflows, China faces growing concerns over financial sector risks. In 2016, net capital outflows from China rose by more than 50 per cent to $725 billion (6.4 per cent of GDP), according to estimates by the Institute of International Finance. In recent months, the Chinese authorities have announced a series of policy measures to curb growing financial vulnerabilities. To mitigate capital outflows, measures taken included raising money market interest rates, strengthening supervision in the foreign exchange market and tightening regulations for investing abroad. Meanwhile, tighter purchase restrictions were imposed in the property market. The authorities also expanded its debt-for-equity swap programme in an effort to contain corporate debt.

Looking ahead, the persistent high uncertainty in the international policy environment could pose considerable headwinds to China?s trade performance and growth. In this aspect, the Chinese authorities will need to continue fine-tuning the policy mix in order to support short-term growth prospects while preserving financial stability.

South Asia: Robust quarterly growth in India, but investment remains subdued

India?s GDP growth maintained a vigorous pace of 7.0 per cent year-on-year in the third quarter of the FY2016/17, supported by robust manufacturing output and a healthy performance of the agricultural sector. The faster-than-expected quarterly growth came amid concerns over the adverse impact of the demonetization policy introduced last November. In fact, the significant credit crunch observed in the economy and other short-term economic indicators suggested a more modest quarterly growth. This apparent paradox partly reflects the substantial difficulties for official growth figures to capture economic activity in the informal sector, which has been most severely affected by the cash crunch. In addition, substantial data revisions to the growth figures in the FY2015/16 also provided a ?base effect? boost to quarterly growth. Official figures confirm that gross fixed capital formation remains largely subdued, weighed down by stressed corporate and bank balance sheets as well as the weak transmission from monetary policy to investment. Recent official data from the Reserve Bank of India also shows that bank credit growth remains weak. In January, bank credit to industry fell by more than 5.0 per cent on a year-on-year basis.

Western Asia: GCC countries agree on a unified VAT

In recent months, Bahrain and Saudi Arabia ratified the Gulf Cooperation Council (GCC)?s Value-Added Tax (VAT) Framework Agreement, which was agreed upon in June 2016. The GCC countries are now expected to implement the unified VAT measure in January 2018. The introduction of this tax is part of the GCC countries? efforts to diversify revenue away from oil. The measure is designed to be introduced in a coordinated manner in order to mitigate any negative impact on intra-GCC trade, following the successful experience of introducing the GCC customs union in the past. The proposed VAT rate is 5 per cent across the board, but special rates for essential goods are still being considered. The net revenue impact is likely to be modest, as the new tax scheme is expected to replace part of customs and excise duties. Once introduced, it would have a one-off impact on the price level in 2018. The magnitude of its impact on inflation is still uncertain as it depends on the markup behaviour of merchants. Given the high degree of uncertainty surrounding the details of its implementation, the introduction of the VAT in the GCC countries may pose considerable operational challenges, but is expected to be a significant milestone for economic diversification.

Latin America and the Caribbean: Argentina and Brazil set to emerge from recession, while Mexico?s economic outlook darkens

Recent data suggest that Argentina?s long-awaited recovery from the recession is finally underway. Economic activity picked up notably in the fourth quarter of 2016, as investment in durable goods and construction recovered. Household consumption has been supported by higher real income, amid gradual disinflation and an increase in credit to the private sector. Meanwhile, Brazil?s worst-ever recession extended into the fourth quarter of 2016, but several leading indicators point to a stabilization of the economy in early 2017. Favourable inflation dynamics, including well-anchored medium-term inflation expectations of around 4.5 per cent, have allowed the Central Bank of Brazil to speed up the pace of interest rate cuts. In February, the monetary authorities reduced the benchmark interest rate by 75 basis points to 12.25 per cent and indicated the possibility of further significant cuts in the coming months. Mexico?s central bank, by contrast, raised its policy rate in February by 50 basis points to 6.25 per cent, the highest level in nearly 8 years. The authorities responded to strong upward price pressures, with inflation accelerating from 3.4 per cent in December to 4.7 per cent in January. This sharp increase in inflation can partly be attributed to a hike in gasoline prices in early 2017, but also reflects the impact of the weaker peso on consumer prices. Amid concerns over the introduction of protectionist measures in the United States, Mexico?s economy showed resilience in the fourth quarter, registering year-on-year growth of 2.4 per cent. However, the economy?s growth prospects for 2017 have further deteriorated, with the central bank downgrading its annual growth forecast to between 1.3 and 2.3 per cent.