Remittances—an important income source for millions of households—have become one of the largest forms of external financing for developing countries, with total inflows in 2023–2024 exceeding the combined value of net foreign direct investment inflows and official development assistance.

Women in developing countries benefit from digital platforms and e-commerce, yet a persistent digital gender gap and high levels of informality continue to exclude many from emerging digital opportunities.

Consumer inflation expectations are shaped by multiple factors—food and energy inflation remain crucial drivers, with persistent and large surges significantly shaping household expectations of inflation across countries.

In a reversal of a decades-long trend, central banks in many developing and some developed countries have increased their gold purchases over the past several years. The purpose of this policy is to enhance the diversity and stability of reserves: the share of the United States dollar in the international reserves of many central banks has been declining.

The U.S. Government’s latest trade policy seeks to address its widening trade deficit, which has recently reached a historic annual high. Persistent trade deficits over the past decades, along with the resulting accumulation of external liabilities to finance them, have long been viewed as a key component of global imbalances.

Following the unprecedented changes in the trade policy of the United States, LDCs must contend simultaneously with significantly higher bilateral tariffs, policy uncertainty, lower growth prospects in many importing countries, a potential re-alignment of supply chains, and a disruption to the existing

multilateral order.

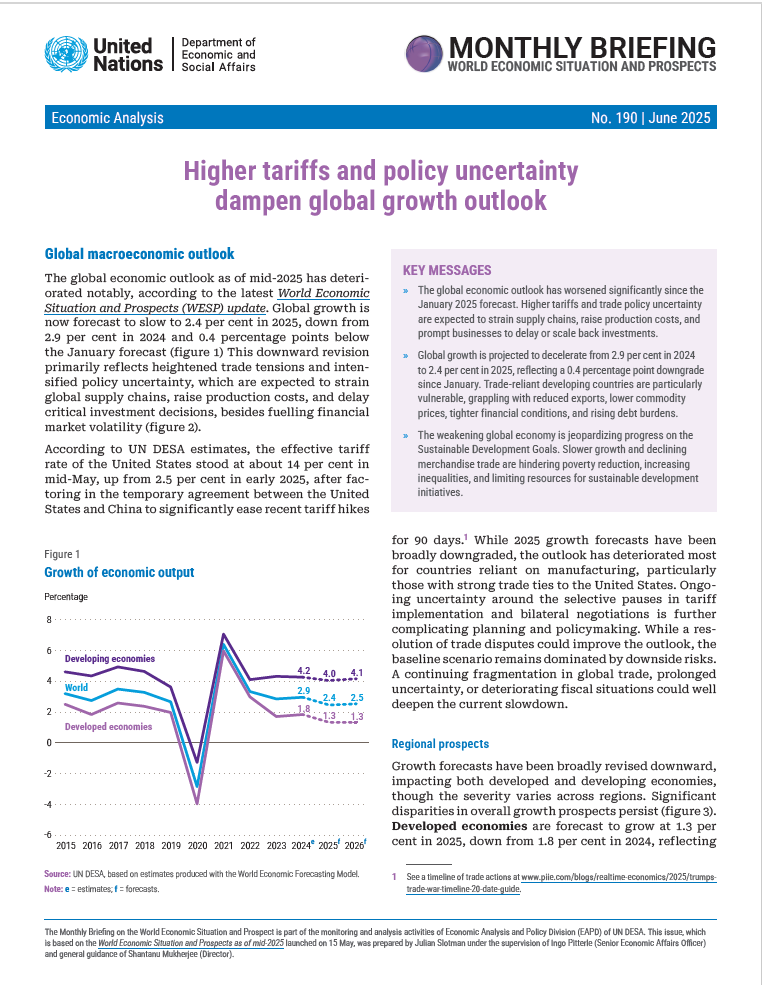

The global economic outlook as of mid-2025 has deteriorated notably, according to the latest World Economic Situation and Prospects (WESP) update. Global growth is now forecast to slow to 2.4 per cent in 2025, down from 2.9 per cent in 2024 and 0.4 percentage points below the January forecast.

Geopolitical fragmentation, trade barriers, and climate change portend recurrent supply-side shocks, fuelling unpredictable inflationary pressures. These disruptions are increasing uncertainty and volatility, which complicate investment decisions and economic policymaking.

The near-term global trade outlook is fraught with uncertainties amid new tariffs and other trade restrictions. While recent history demonstrates that the global trading system is resilient, often adapting by finding alternative channels for sustaining commerce, policy uncertainty could hinder this process by discouraging necessary investments.

The world economy has shown resilience despite multiple shocks, but the outlook remains uncertain due to ongoing conflicts, geopolitical and trade tensions, climate risks, and mounting fiscal pressures.

Welcome to the United Nations

Welcome to the United Nations