Economic growth in landlocked developing countries (LLDCs) is expected to be steady in the near term but remains well below the average in the pre-pandemic decade. Substantial downside risks remain, including commodity price volatility, debt challenges, climate disasters and geopolitical tensions.

According to the World Social Report 2024, urgent global action is needed to support national efforts to address the setbacks caused by the recent global crises, and to avoid the conversion of future shocks to crises. The report explains that, in our current global policy environment, shocks more readily turn into crises that cross boundaries, demanding international action. Particularly as such crises disproportionately impact the most vulnerable people, societies and countries.

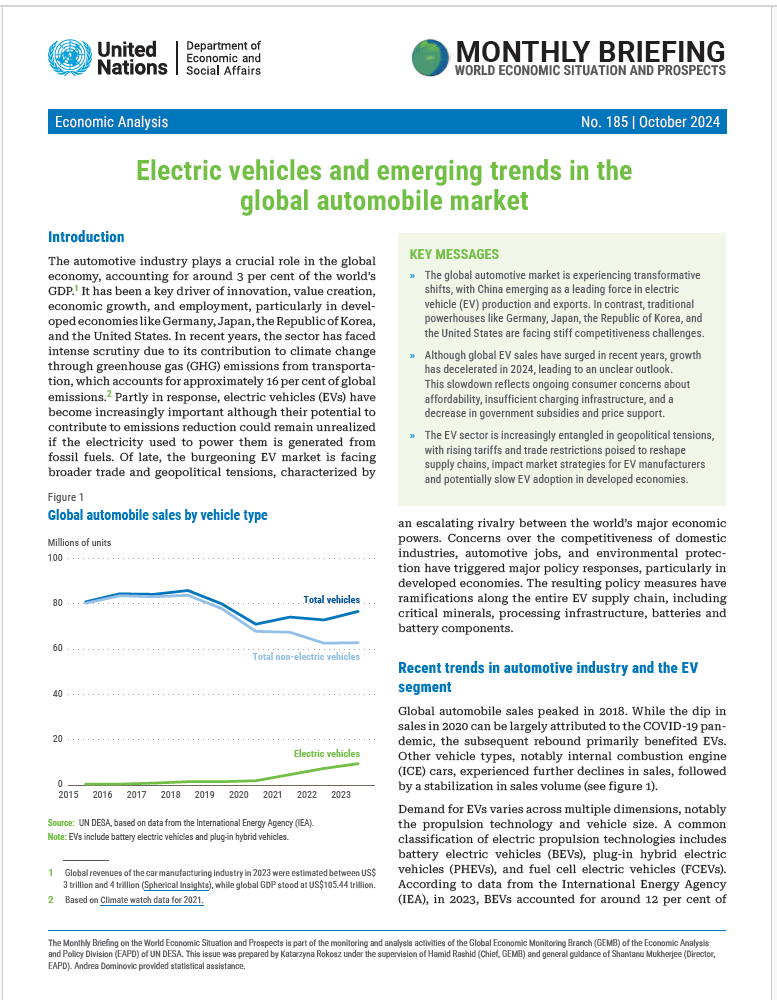

The global automotive market is experiencing transformative shifts, with China emerging as a leading force in electric vehicle (EV) production and exports. In contrast, traditional powerhouses like Germany, Japan, the Republic of Korea, and the United States are facing stiff competitiveness challenges.

Potential impacts of LDC graduation: Cambodia, Comoros, Djibouti, Senegal and Zambia

Impacts of LDC Graduation on Trade-Related Aspects of Intellectual Property Rights (TRIPS) in Cambodia, Djibouti, Senegal and Zambia

Updated impact assessment for Solomon Islands

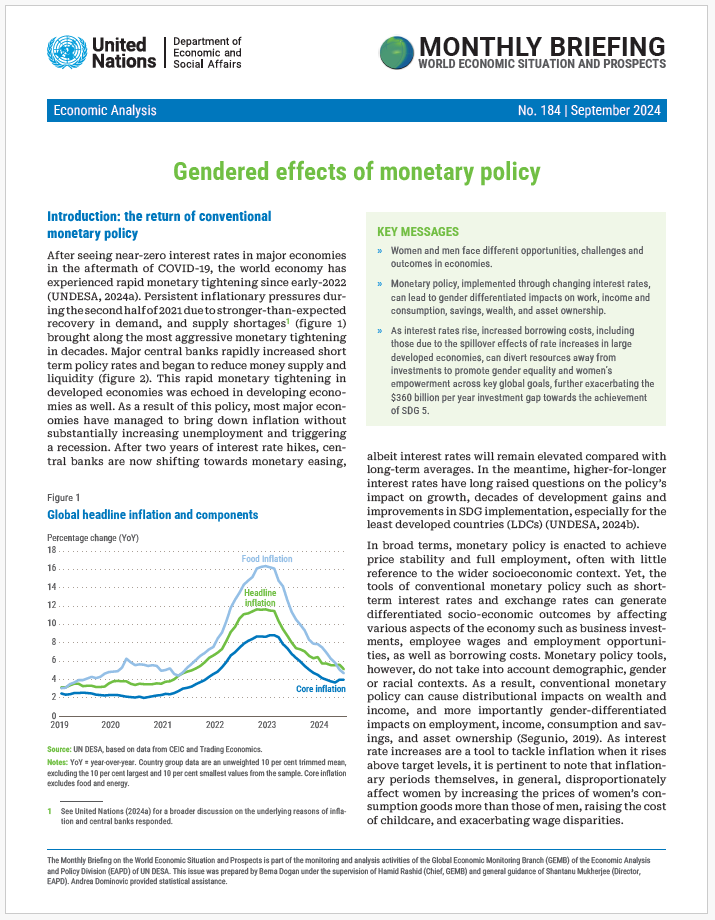

After seeing near-zero interest rates in major economies in the aftermath of COVID-19, the world economy has experienced rapid monetary tightening since early-2022 (UNDESA, 2024a). Persistent inflationary pressures during the second half of 2021 due to stronger-than-expected recovery in demand, and supply shortages brought along the most aggressive monetary tightening in decades.

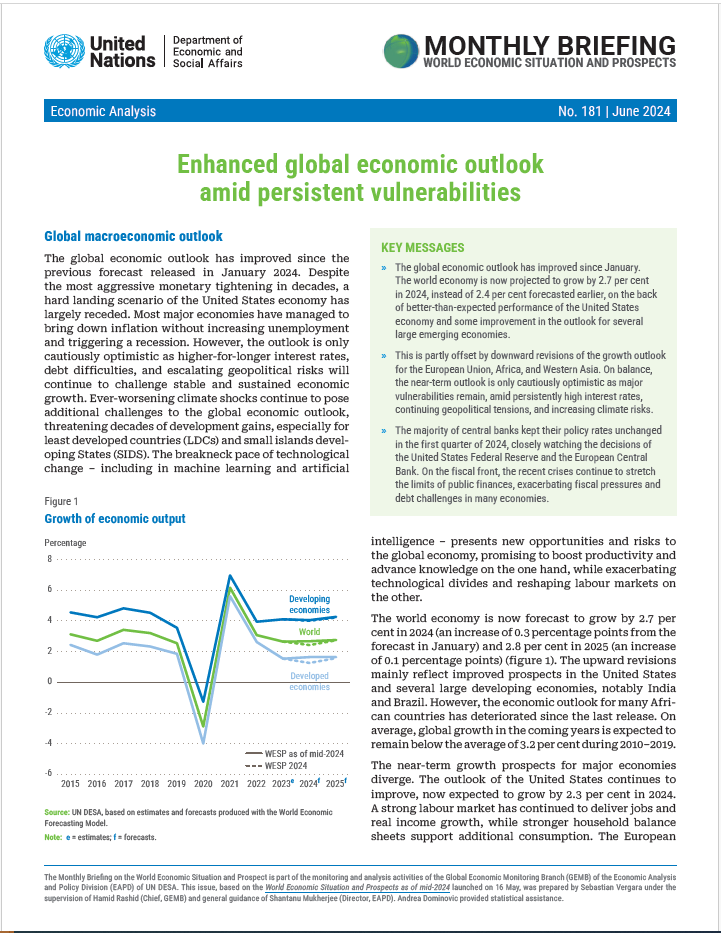

After years of turbulence and significant volatility in economic output, the world economy is on a more stable trajectory. Global growth performance has held up surprisingly well in the face of recent shocks, including aggressive interest rate hikes by major central banks during 2022–2023 and an escalation of conflicts with international spillovers. Robust consumer spending in several large developed and developing economies – buoyed by high levels of employment, rising real wages, and relatively healthy household balance sheets – has sustained economic resilience.

On 1 May 2004, eight countries from Eastern Europe – the Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Slovakia and Slovenia – the group often referred to as EU-8, along with Cyprus and Malta, became full-fledged members of the European Union (EU). This event is often called the “Big Bang” enlargement of the EU, with the set of pre-existing members being referred to as the EU-15.

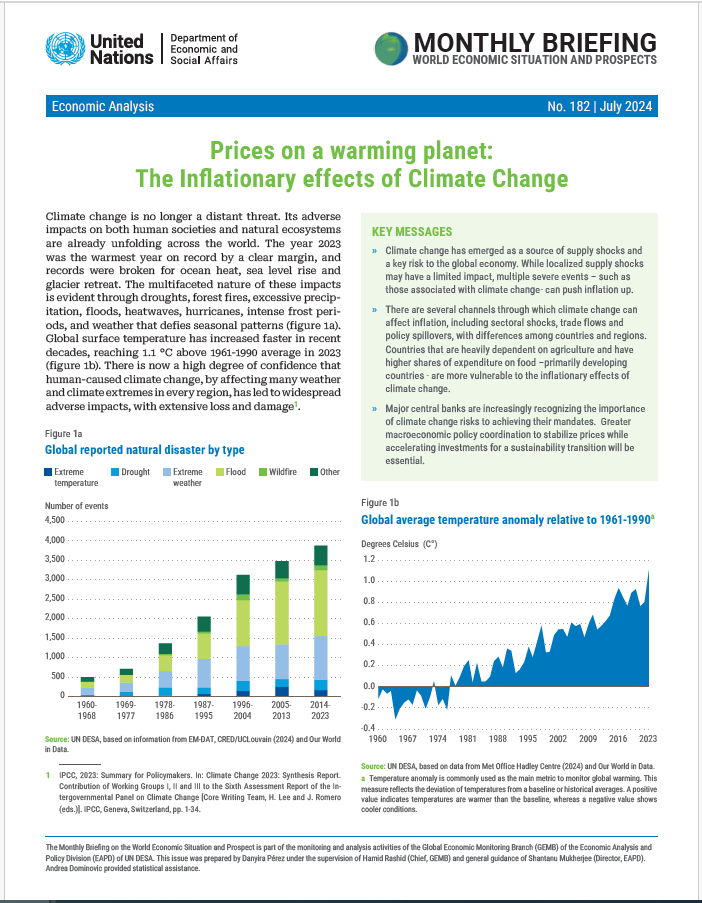

Climate change has emerged as a source of supply shocks and a key risk to the global economy. While localized supply shocks may have a limited impact, multiple severe events – such as those associated with climate change- can push inflation up.

The majority of central banks kept their policy rates unchanged in the first quarter of 2024, closely watching the decisions of the United States Federal Reserve and the European Central Bank.

The Handbook on the Least Developed Country Category contains comprehensive and authoritative information on criteria defining the category, graduation procedures, and international support measures for LDCs. This revised edition reflects recent developments in the LDC category, including refinements to the LDC criteria and the progress of several countries towards graduation from the category.

Welcome to the United Nations

Welcome to the United Nations